Table of Contents

Most companies don’t realize their financial software vendor was the wrong choice until six months into the build. By then, the damage is structural. Compliance gaps were missed during scoping. Integration debt from a codebase never designed for regulated environments. Settlement logic nobody flagged until transactions started failing at scale.

Frozen accounts, broken reconciliation, and erratic fraud management don’t appear in a proposal deck. They appear in a post-launch incident report.

The 2026 fintech market has no shortage of vendors claiming expertise. What separates a capable build partner from one who simply presents well comes down to a handful of questions asked before the contract is signed. About compliance architecture, data residency, role-based access controls, and failure handling at the transaction level.

The companies getting this right aren’t the ones with the biggest budgets. They’re the ones who evaluated smarter, earlier.

This guide gives product and technology leaders that exact framework, built from real delivery patterns across banking, lending, insurance, and investment platforms. Use it whether you’re building your first payment module or re-platforming a core banking layer.

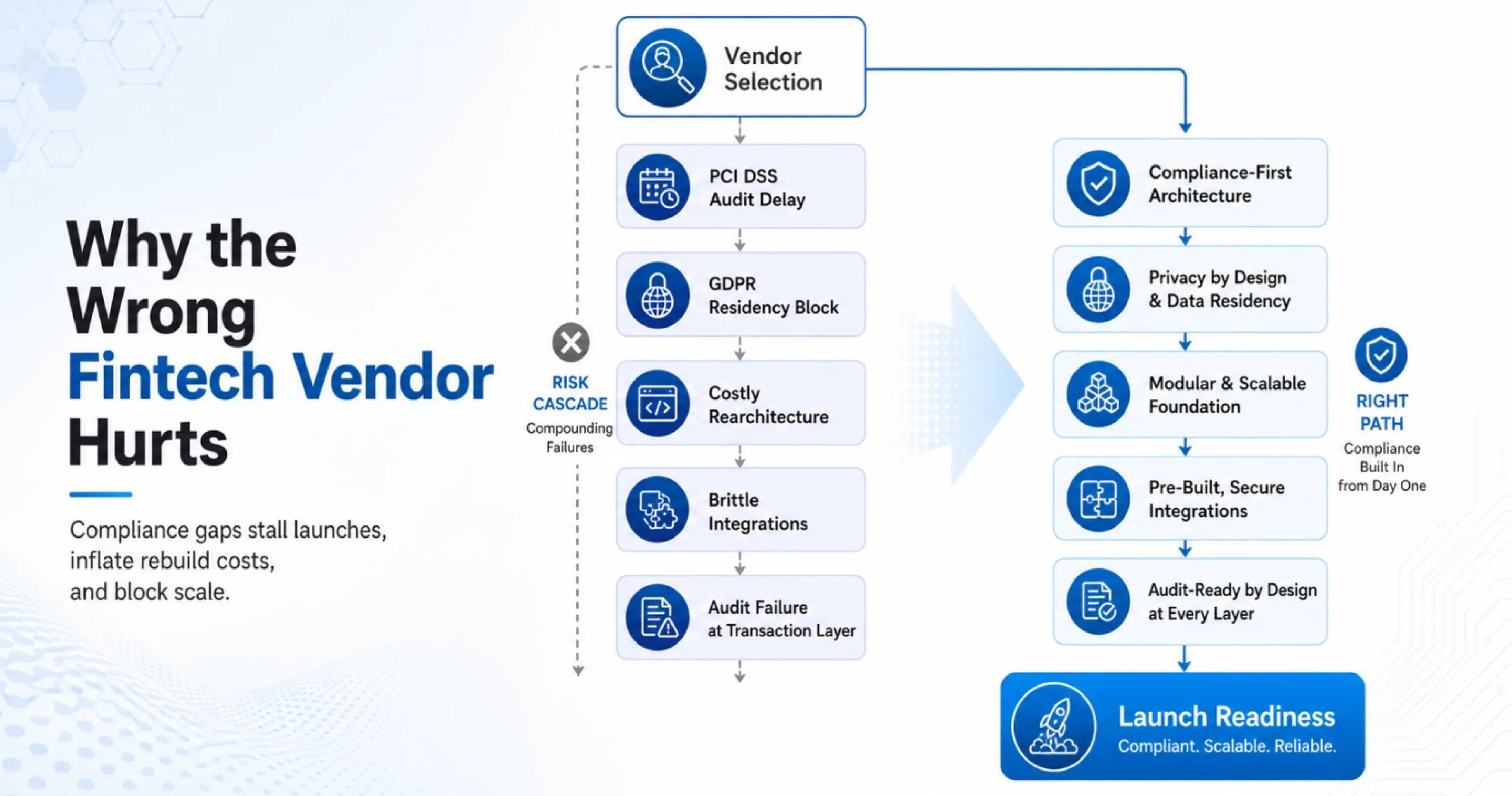

Why the Wrong Financial Software Development Company Hurts

Regulatory failure in fintech isn’t a fine you pay and move on from. It’s a pause button on your entire go-to-market. In fact, 73% of fintech startups fail within their first three years, specifically due to preventable regulatory compliance issues, according to a 2025 study by Hare Strategy Group.

The compounding cost of the wrong vendor:

- Missed PCI DSS requirement: triggers a full audit cycle, stalling your launch timeline

- GDPR gap in data residency: blocks EU market expansion entirely, not temporarily

- Features built before compliance mapping: forces rearchitecting decisions that typically cost more than the original build

- Brittle third-party integrations: undocumented, unowned, and unresolvable once the vendor exits

- Compliance logic in the wrong layer: buried in reporting instead of the transaction layer, it looks compliant in dashboards but fails under audit

These aren’t edge cases. They’re the most common reasons fintech builds stall, overspend, or get shelved before launch.

The right financial software development company treats compliance as an input to architecture, not an output of QA. That distinction affects your audit readiness, your cost of ownership, and your ability to scale without rebuilding.

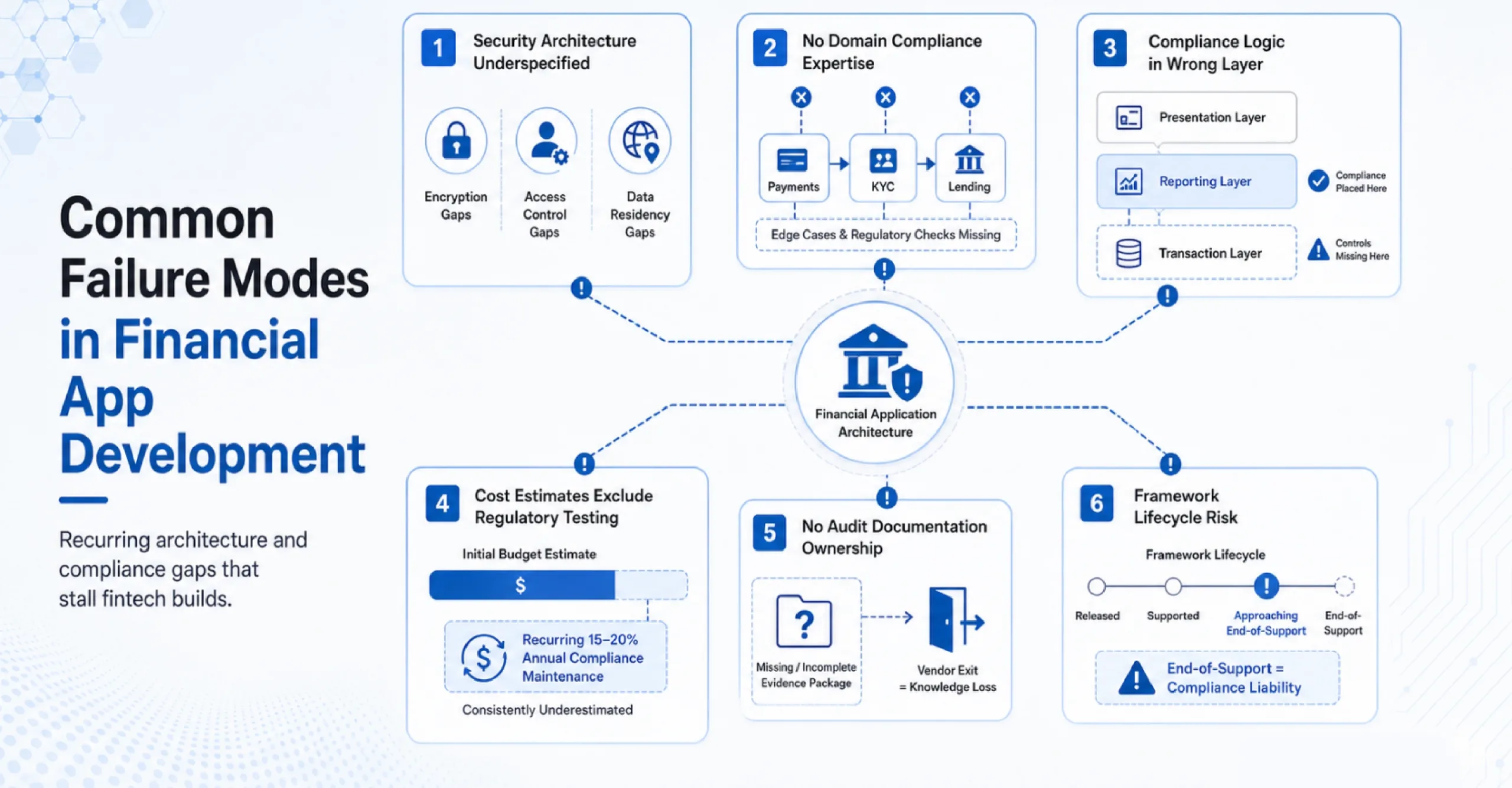

Common Failure Modes in Financial Application Development

These patterns appear repeatedly across failed or stalled fintech builds:

- Security architecture underspecified at the design phase: Encryption standards, access controls, and data residency left as implementation details rather than architectural constraints

- Engineering teams without domain compliance knowledge: Developers who haven’t built payment engines, KYC flows, or lending origination systems miss edge cases that domain specialists catch immediately

- Compliance logic placed in the wrong layer: Built into reporting instead of the transaction layer, creating a system that looks compliant in dashboards but fails under audit

- Cost estimates that exclude regulatory testing cycles: Budget for ongoing compliance maintenance runs 15 to 20% of the initial build cost annually; vendors who exclude this are not quoting the real number

- No defined audit documentation ownership: When the vendor exits, the client inherits undocumented systems with no evidence package for regulators

- Frameworks chosen without evaluating support lifecycles: Stack decisions in fintech carry long-term consequences; a framework approaching end-of-support becomes a compliance liability, not just a technical one

Key Criteria for Evaluating Financial Software Development Services

Use the table below as a baseline evaluation grid. Adjust weights for your specific compliance jurisdiction and product type.

What a Reliable Financial Software Development Company Looks Like

A strong financial software development company does not just write code. It manages risk at every layer of the product lifecycle. Compliance is built into the architecture. It is not patched in after QA flags an issue.

Compliance-First Architecture

Every custom fintech software development project has a regulatory ceiling. The financial software development company you choose must understand that ceiling before writing a single line.

Domain-Matched Engineering Teams

Fintech software solutions fail when the engineering team does not understand financial workflows. A developer who has never built a ledger reconciliation module will miss edge cases that a domain expert catches immediately.

Look for a financial software development company whose engineers have shipped payment engines, KYC flows, or lending origination systems before.

Transparent Custom Financial Software Development Timelines

Regulatory cycles add time. Any financial software development company that gives you a timeline without accounting for compliance testing is not being straight with you.

Custom financial software development projects in regulated environments need buffer sprints built into the plan. Demand a schedule that explicitly names each compliance milestone.

Generalist vs Specialist: Choosing the Right Financial Software Development Services

Not all financial software development services are equivalent. Generalist shops can handle the code. Specialist financial software development companies handle the code and the compliance, and the domain logic simultaneously. Here is a direct comparison.

How to Vet a Financial Software Development Company Before Signing

The vendor pitch is not sufficient evidence. You need to run a structured vetting process. These steps significantly reduce the risk of a bad financial software development engagement.

Step 1: Request a Compliance Architecture Review

Ask the financial software development company to walk you through how they handle data residency, encryption at rest, and access control in a live financial product. A company with genuine custom fintech software development depth will answer this without hesitation. Vague responses are a signal.

Step 2: Examine Financial Application Development Case Studies

Generic case studies with no named outcomes are not evidence. Demand financial application development case studies with specific metrics. Time to compliance sign-off, defect rates in regulated modules, API uptime in production. A credible financial software development company has these numbers.

Step 3: Assess the Custom Financial Software Development Team Roster

Who actually works on your project matters. Ask for CVs of the lead architect and compliance engineer. Confirm they have delivered custom financial software development in your specific vertical. Staff augmentation models sometimes swap people mid-engagement. Get contractual guarantees on team continuity.

Step 4: Evaluate Fintech Software Solutions Tech Stack Choices

Stack decisions in fintech software solutions carry long-term consequences. A financial software development company that defaults to the newest framework without evaluating the support lifecycle is creating future technical debt for you. Ask why they chose a particular stack for your use case. The reasoning matters as much as the choice.

How Ace Infoway Delivers Financial Software Development Services

Ace Infoway delivers financial software development for banking, insurance, lending, and investment management clients through a structured three-phase model:

Phase 1: Architecture and Compliance Mapping

Every engagement starts with a discovery sprint. Regulatory obligations are mapped, data flow boundaries defined, and a compliance architecture document produced before a single line of code is written. That document governs every build decision that follows.

Phase 2: Agile Build with Compliance-Gate Sprints

Each squad includes domain-specialist engineers, a dedicated QA lead for regulatory testing, and a compliance reviewer who signs off on every sprint deliverable. The output is audit-ready at every stage, not just at go-live.

Phase 3: Post-Launch Support with Regulatory Update Cycles

Fintech software solutions from Ace Infoway are built on proven, long-support-window stacks. Integration partners include core banking platforms, payment gateways, KYC providers, and cloud-native infrastructure layers.

Questions to Ask Every Financial Software Development Company

Use this list in your RFP process or vendor calls. The quality of answers reveals more than the portfolio.

Conclusion

The financial software development company you choose in 2026 is a strategic partner, not a code vendor. Compliance complexity is rising. Regulatory cycles are shortening. The margin for error in financial software development services is narrowing.

A specialist financial software development company that understands your domain, embeds compliance from day one, and maintains your product through regulatory change cycles is the asset you need.

Ace Infoway has delivered custom fintech software development for regulated financial products across multiple markets.

If your next build or modernization project involves financial application development at any scale, the evaluation framework above is your starting point. Use it to filter vendors fast and make a decision you can defend to your board and your auditors.

Frequently Asked Questions

What separates a financial software development company from a general software agency?

A specialist financial software development company embeds compliance expertise directly into the engineering team rather than treating compliance as a separate legal review. This allows regulatory requirements such as PCI DSS, SOC 2, GDPR, and industry-specific standards to influence architecture decisions from the beginning. General software agencies can build functional products, but they often lack the fintech domain knowledge needed to avoid costly compliance gaps and rework later in the project lifecycle.

How much do custom fintech software development projects typically cost?

Custom fintech software development costs vary based on project scope, compliance requirements, integrations, and product complexity. A payment gateway integration for a startup may require a significantly different investment than an enterprise-scale banking modernization initiative. Businesses should focus on total cost of ownership rather than hourly rates and ensure vendors include regulatory testing, compliance reviews, maintenance, and support in their pricing models.

How long does financial application development take for a regulated product?

Financial application development timelines depend on regulatory obligations, system integrations, and product complexity. A lending platform module may take 12 to 20 weeks, while a multi-market payment platform with cross-border compliance requirements can take considerably longer. The most efficient financial software development companies integrate compliance testing into every sprint, reducing delays and avoiding extensive remediation before launch.

What should I look for in custom financial software development security practices?

Strong custom financial software development starts with threat modeling before architecture decisions are made. Key security practices include encryption at rest and in transit, role-based access control, least-privilege permissions, defined data residency policies, secure API management, and comprehensive penetration testing before deployment. Reviewing previous security architecture documentation can help validate a vendor’s expertise beyond marketing claims.

Can a financial software development company handle ongoing compliance updates after launch?

Yes. Ongoing compliance support should be included as part of a formal service-level agreement. Financial regulations evolve continuously, including updates to PCI DSS standards, regional banking requirements, and data protection laws. A reliable financial software development company provides proactive compliance monitoring, regulatory update implementation, and dedicated post-launch support to keep financial applications secure, compliant, and audit-ready.